[ad_1]

You will have contributed to a Roth IRA after which realized later within the yr that you’d exceed the revenue restrict. You recharacterized the Roth IRA contribution as a Conventional IRA contribution and transformed it to Roth once more earlier than the tip of the yr. Your IRA custodian despatched you two 1099-R varieties, one for the recharacterization and one for the conversion. This put up exhibits you find out how to put them into the H&R Block tax software program.

For those who had performed the recharacterizing and changing within the following yr, you would need to break up the tax reporting into two years by following Break up-12 months Backdoor Roth IRA in H&R Block, 1st 12 months and Break up-12 months Backdoor Roth IRA in H&R Block, 2nd 12 months. Now since you caught the issue quickly sufficient earlier than the tip of the yr, you’ll be able to deal with all of it in the identical yr by following this information.

Right here’s the instance situation we’ll use on this information:

You contributed $6,500 to a Roth IRA for 2023 in 2023. You realized that your revenue could be too excessive later in 2023. You recharacterized the Roth contribution for 2023 as a Conventional contribution. The IRA custodian moved $6,600 out of your Roth IRA to your Conventional IRA as a result of your authentic $6,500 contribution had some earnings. The worth elevated once more to $6,700 while you transformed it to Roth earlier than December 31, 2023. You acquired two 1099-R varieties, one for $6,600 and one other for $6,700.

For those who didn’t do any of those recharacterizing and changing, please observe our information for a “clear” backdoor Roth in The way to Report Backdoor Roth in H&R Block Tax Software program.

For those who’re married and each you and your partner did the identical factor, you must observe the steps under as soon as for your self and as soon as once more to your partner.

Use H&R Block Obtain Software program

The screenshots under are taken from H&R Block Deluxe downloaded software program. The downloaded software program is each inexpensive and extra highly effective than H&R Block’s on-line software program. For those who haven’t paid to your H&R Block On-line submitting but, contemplate shopping for H&R Block obtain software program from Amazon, Walmart, Newegg, and lots of different locations. For those who’re already too far in getting into your information into H&R Block On-line, make this your final yr of utilizing H&R Block On-line. Change over to H&R Block obtain software program subsequent yr.

1099-R for Recharacterization

We deal with the 1099-R kind for the recharacterization first. This 1099-R kind has a code “N” in Field 7.

Click on on Federal -> Revenue. Scroll down and discover IRA and Pension Revenue (Kind 1099-R). Click on on “Go To.”

Click on on Import 1099-R for those who’d like. I present handbook entries with “Enter Manually” right here.

Only a common 1099-R.

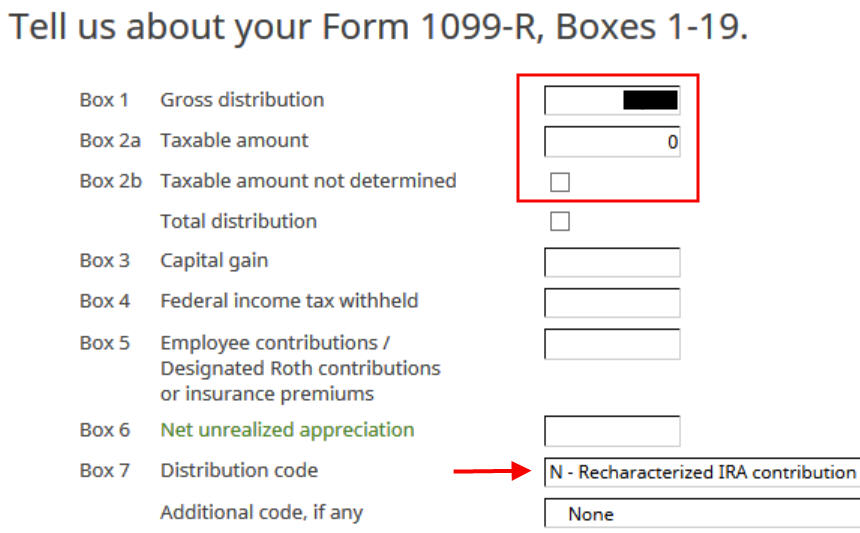

The 1099-R kind for the recharacterization exhibits the quantity moved from the Roth IRA to the Conventional IRA in Field 1. The taxable quantity is 0 in Field 2a and the “Taxable quantity not decided” field isn’t checked. The code in Field 7 is “N.”

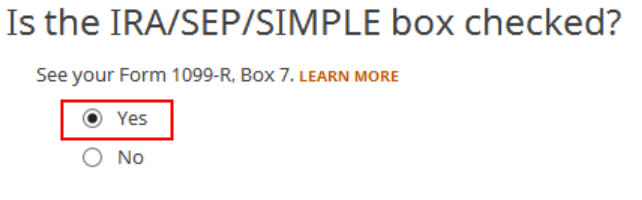

The “IRA/SEP/SIMPLE” field might or is probably not checked in your kind. It isn’t checked in our kind.

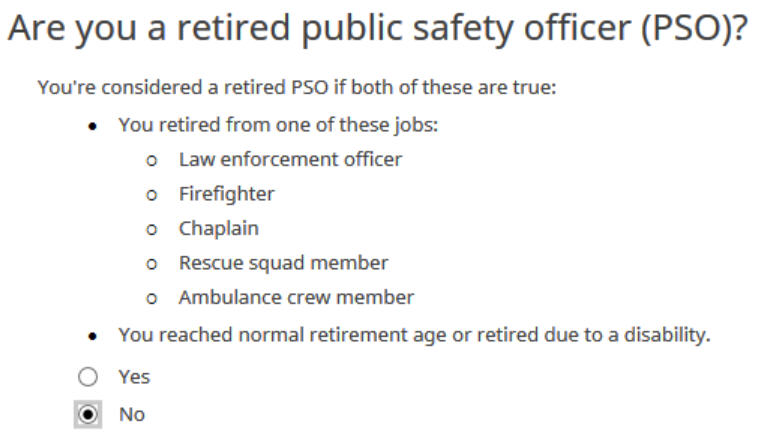

Not a retired public security officer.

We like to listen to that.

You’re performed with the primary 1099-R kind. Click on on “Enter Manually” so as to add the second for those who don’t have already got each 1099-R varieties imported.

1099-R for Conversion

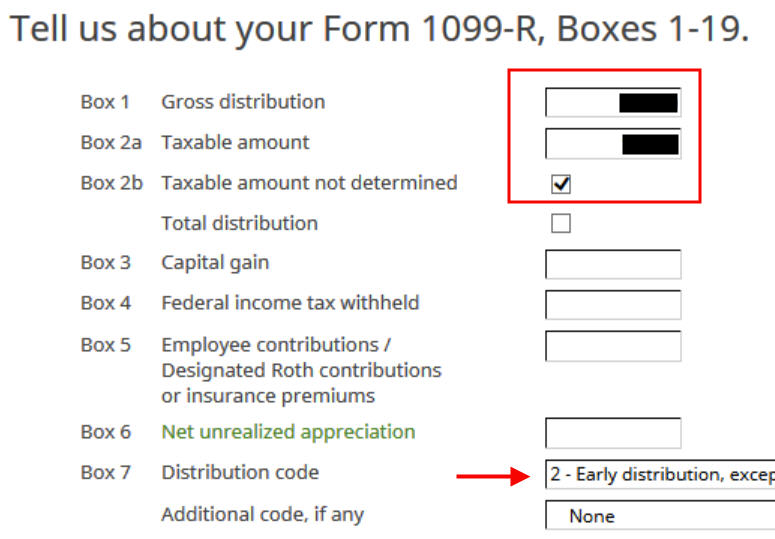

The 1099-R for the Roth conversion has both a code “2” or code “7” in Field 7.

The second 1099-R kind can also be a daily 1099-R.

It’s regular to see the conversion reported in Field 2a because the taxable quantity when Field 2b is checked to say “Taxable quantity not decided.” The code in Field 7 is “2″ while you’re below 59-1/2 or “7” while you’re over 59-1/2.

The “IRA/SEP/SIMPLE” field is checked on this 1099-R kind for the Roth conversion.

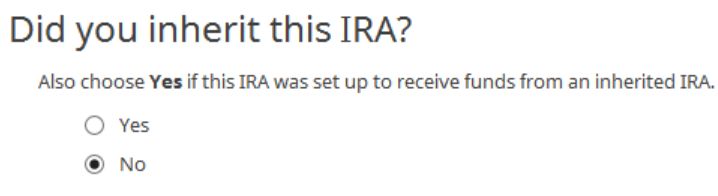

Didn’t inherit it.

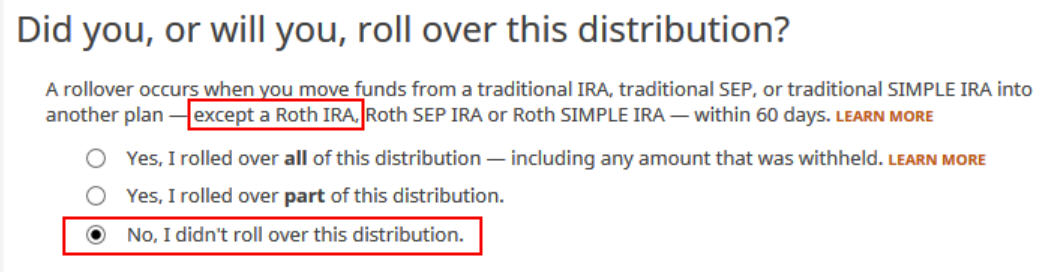

Transformed, Did Not Roll Over

This is a vital query. Learn rigorously. Reply No, since you transformed, not rolled over.

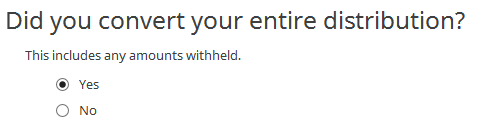

Now reply Sure, you transformed.

We transformed all of it.

It’s safer to reply “Sure” right here as a result of you’ll be able to all the time say your foundation was zero when the software program asks you what it was.

The refund meter drops lots at this level. Don’t panic. It’s regular and solely non permanent. It is going to come again up after we proceed.

You’re performed with one 1099-R. Repeat the above in case you have one other 1099-R. For those who’re married and each of you transformed to Roth, take note of whose 1099-R it’s while you enter the second. You’ll have issues for those who assign each 1099-R’s to the identical particular person once they belong to every partner. Click on on “Completed” if you end up performed with all of the 1099-Rs.

H&R Block has a number of extra questions.

The wording is complicated right here however you must reply “Sure.” You recharacterized a Roth IRA contribution as a Conventional IRA contribution. It counts.

H&R Block will wait till you additionally enter your 2023 contribution. Your refund meter remains to be depressed however don’t fear.

Roth IRA Contribution Recharacterized to Conventional

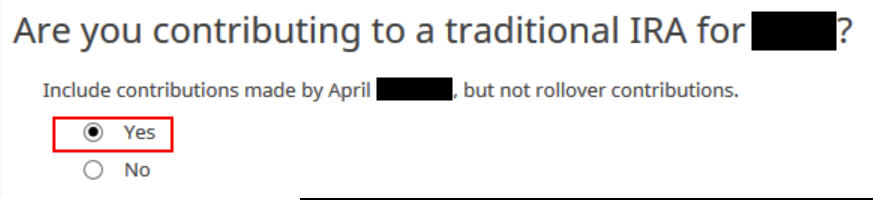

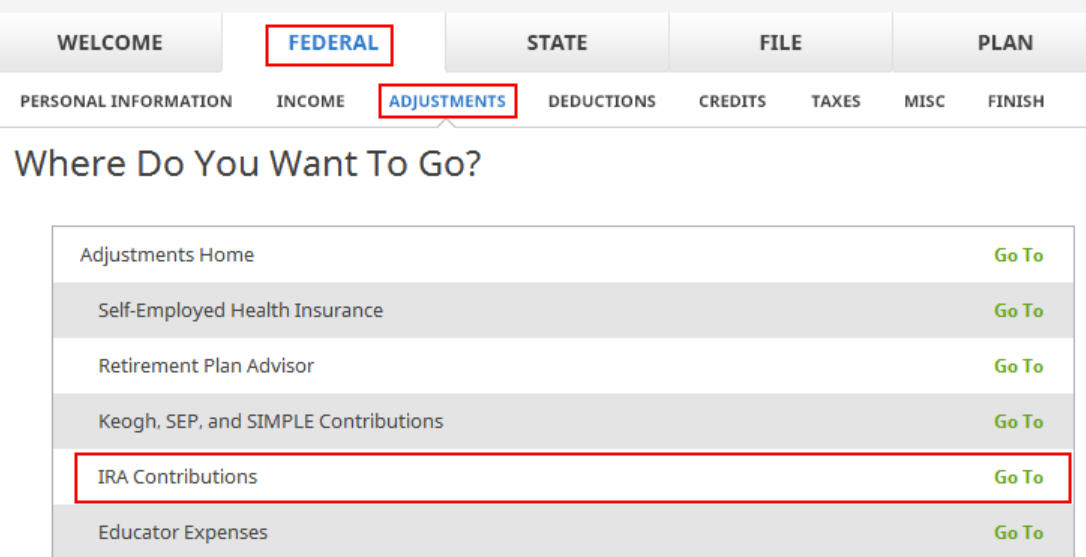

Click on on Federal -> Changes. Discover IRA Contributions. Click on on “Go To.”

Reply “Sure” since you contributed to an IRA for the yr in query.

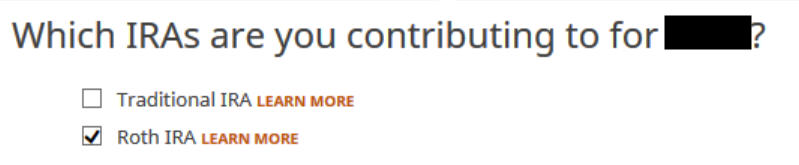

Verify the field for Roth IRA since you initially contributed to a Roth IRA earlier than you recharacterized your contribution.

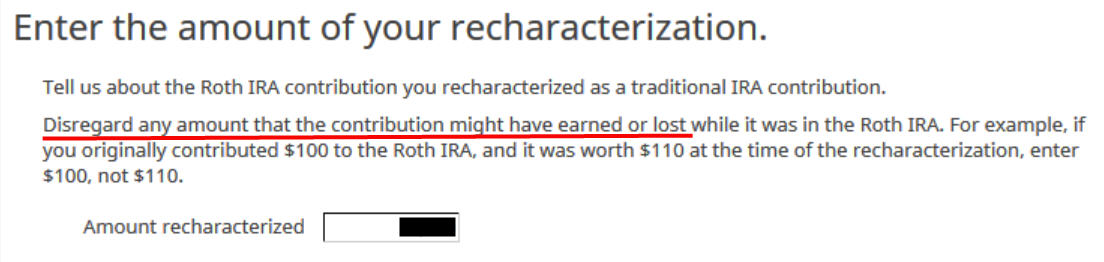

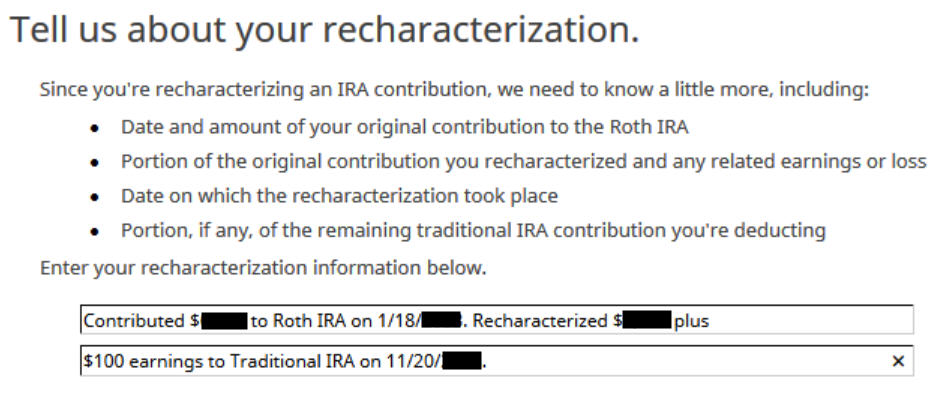

Enter your authentic contribution quantity. It’s $6,500 in our instance.

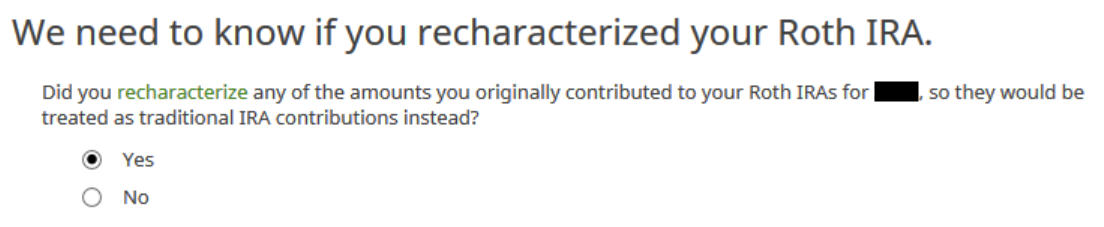

Reply Sure since you recharacterized the contribution.

The quantity right here is relative to the unique contribution quantity. For those who recharacterized the entire thing, enter $6,500 in our instance, not $6,600 which was the quantity with earnings that the IRA custodian moved into the Conventional IRA.

The IRS requires a quick assertion to explain your recharacterization.

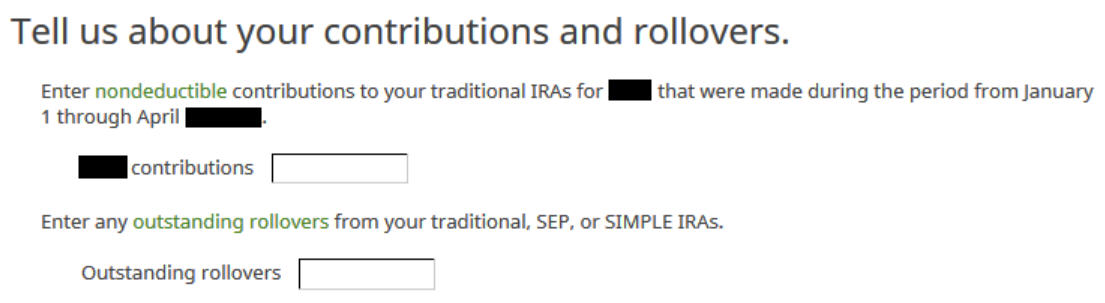

Go away the packing containers clean since you recharacterized earlier than the tip of 2023.

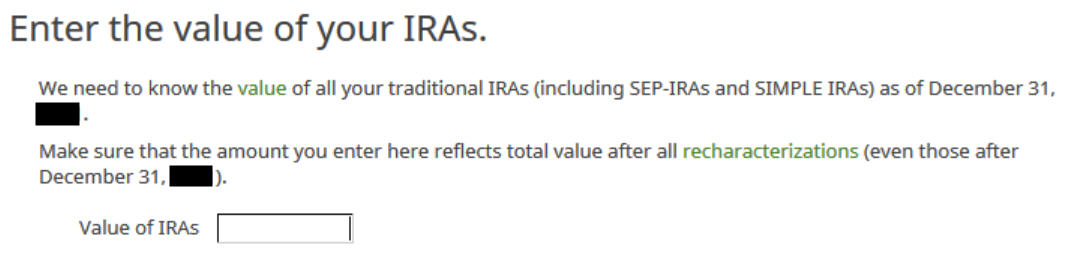

The field must be clean or zero while you emptied all of your Conventional IRAs after changing 100% to Roth. For those who had a number of {dollars} of earnings after you transformed and also you left them within the account, get the worth out of your year-end statements and put it right here. The software program will apply the pro-rata rule.

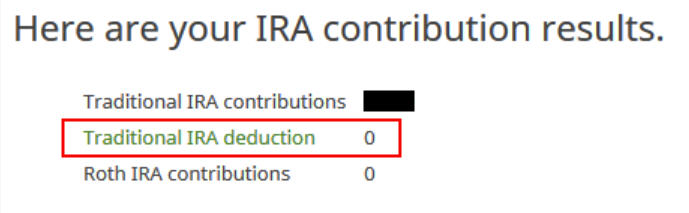

No extra contribution.

0 in Conventional IRA deduction means it’s nondeductible. For those who see a deduction right here it means the software program thinks you qualify for a deduction. You don’t have a alternative to say no the deduction. Click on on Subsequent. Repeat to your partner if each of you contributed to a Roth IRA for 2023 after which recharacterized earlier than the tip of 2023.

Now the refund meter ought to return up.

Taxable Revenue

You’re performed with the 2 1099-R varieties and your Roth IRA contribution recharacterized to Conventional. Let’s take a look at how they present up in your tax return. Click on on Kinds on the highest and open Kind 1040 and Schedules 1-3. Click on on Conceal Mini WS. Scroll all the way down to strains 4a and 4b.

Line 4a exhibits the sum of your two 1099-R varieties. It’s $13,300 in our instance ($6,600 recharacterization plus $6,700 conversion). That is regular. Line 4b exhibits that $201 is taxable after we count on it to be the $200 in earnings (contributed $6,500, transformed $6,700). That is additionally regular as a consequence of rounding.

Kind 8606 exhibits these for our instance:

| Line # | Quantity |

|---|---|

| 1 | 6,500 |

| 3 | 6,500 |

| 5 | 6,500 |

| 13 | 6,499 (as a consequence of rounding, must be 6,500) |

| 14 | 1 (as a consequence of rounding, must be 0) |

| 16 | 6,700 |

| 17 | 6,499 (as a consequence of rounding, must be 6,500) |

| 18 | 201 (as a consequence of rounding, must be 200) |

Change to Clear Backdoor Roth

You prevented having to separate your IRA contribution and Roth conversion in two completely different tax returns by recharacterizing in the identical yr and changing earlier than December 31. Nonetheless, you needed to do the additional work together with your IRA custodian and observe all these steps on this information while you do your taxes.

It’s significantly better to go along with a “clear” backdoor Roth from the get-go. If there’s any chance that your revenue might be over the restrict once more, merely contribute to a Conventional IRA for 2024 in 2024 and convert it to Roth in 2024.

You’re allowed to do a clear backdoor Roth even when your revenue finally ends up under the revenue restrict for a direct contribution to a Roth IRA. It’s a lot easier than the complicated recharacterize-and-convert maneuver. You then solely have to observe our information for a clear backdoor Roth in The way to Report Backdoor Roth in H&R Block Tax Software program.

Troubleshooting

For those who adopted the steps and you aren’t getting the anticipated outcomes, right here are some things to verify.

Contemporary Begin

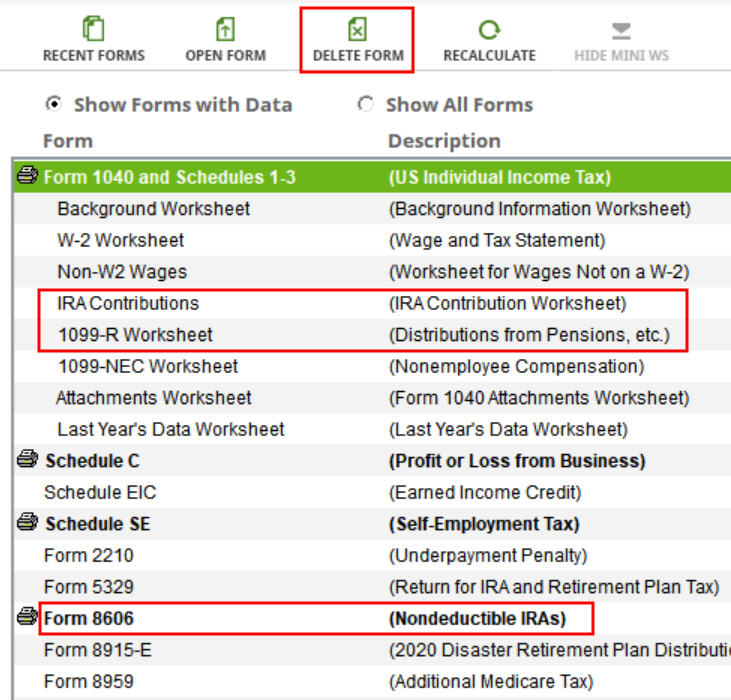

It’s greatest to observe the steps contemporary in a single move. For those who already went forwards and backwards with completely different solutions earlier than you discovered this information, a few of your earlier solutions could also be caught someplace you now not see. You may delete them and begin over.

Click on on Kinds and delete IRA Contributions Worksheet, 1099-R Worksheet, and Kind 8606. Then begin over by following the steps right here.

Conversion Is Taxed

For those who don’t have a retirement plan at work, you’ve gotten a better revenue restrict to take a deduction in your Conventional IRA contribution. In case you have a retirement plan at work however your revenue is low sufficient, you might be additionally eligible for a deduction in your Conventional IRA contribution. The software program provides you the deduction if it sees that your revenue qualifies. It doesn’t provide the alternative of constructing it non-deductible. You see this deduction on Schedule 1 Line 20.

Taking this deduction makes your conversion taxable. The taxable Roth IRA conversion and the deduction to your Conventional IRA contribution offset one another to create a wash. That is regular and it doesn’t trigger any issues while you certainly don’t have a retirement plan at work or when your revenue is sufficiently low.

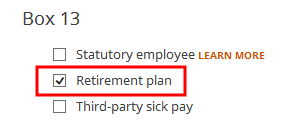

For those who even have a retirement plan at work, perhaps the software program didn’t see it. Whether or not you’ve gotten a retirement plan at work is marked by the “Retirement plan” field in Field 13 of your W-2. Perhaps you forgot the verify it while you entered the W-2. Double-check the “Retirement plan” field in Field 13 of your (and your partner’s) W-2 entries to verify it matches the W-2.

Say No To Administration Charges

If you’re paying an advisor a share of your property, you might be paying 5-10x an excessive amount of. Learn to discover an unbiased advisor, pay for recommendation, and solely the recommendation.

[ad_2]