[ad_1]

Mortgages may be seen very otherwise.

Some see them as a constructive monetary instrument, a solution to release their cash so it may be invested elsewhere, ideally for a greater return.

Then there are those that view mortgages as the foundation of all evil, as a debt overhang that should be terminated as rapidly as doable.

No matter your stance, you’ve in all probability entertained the thought of constructing “additional mortgage funds,” although it’s possible you’ll not know the precise affect, because of the complexity of mortgage amortization.

Happily, there are early payoff calculators out there that take the guesswork out of the method and make it straightforward to see how a lot it can save you in a variety of totally different situations.

Including an Further Mortgage Cost of $10 Per Month

- Even including a nominal quantity comparable to $5 or $10

- On a month-to-month foundation over an extended time frame

- Can prevent 1000’s of {dollars} in your mortgage

- And shorten your mortgage time period on the identical time

Let’s begin with a easy situation the place you add simply $10 a month in additional cost to principal.

Assuming you’ve received a $100,000 mortgage quantity set at 4% on a 30-year fastened mortgage, that additional $10 cost would prevent $3,191.81 over the complete mortgage time period.

It might additionally shorten your mortgage by 13 months, which means your 30-year mortgage could be a 28-year (ish) mortgage.

In order that’s excellent news, proper? You save 1000’s and also you solely should pay a measly $10 additional per 30 days. You in all probability wouldn’t even discover the distinction.

What when you bumped up that additional cost to $25? Nicely, you’d shave 32 months off your mortgage, almost three years, and cut back whole curiosity by $7,450.04.

Feeling formidable? Add $100 a month and also you cut back your time period by 101 months, or almost 8.5 years, whereas saving $22,463.79 in curiosity.

You can even simply make your mortgage funds a strong spherical quantity and lower your expenses that method too.

The world is your oyster actually, as long as your mortgage servicer understands and accepts that these funds are to go towards the excellent principal stability.

Talking of, make sure that it’s very clear that any additional funds go to the proper place. Usually, you possibly can’t make break up funds, or funds for lower than the whole quantity due.

So any additional must be on prime of the minimal quantity due for the month.

Some servicers will allow you to point out the place the additional ought to go, comparable to towards your escrow account or the principal stability.

In case your objective is to pay the mortgage down quicker, you’ll need it to go towards the principal stability.

Tip: In the event you can’t decide to the upper month-to-month funds related to a 15-year fastened mortgage, additional funds may present related financial savings on a 30-year fastened.

Further Mortgage Funds Are Extra Worthwhile Early On

- You get extra worth out of additional mortgage funds early on within the mortgage time period

- As a result of the excellent stability is bigger on the outset

- And early funds are composed principally of curiosity (front-loaded)

- Any additional funds will decrease future curiosity for the remaining months, which will probably be extra plentiful when you make them throughout the early years

As you possibly can see, it’s not that tough to save lots of a ton of cash by way of additional mortgage funds, but it surely additionally issues whenever you begin making these extra funds.

Utilizing our $100 instance, when you began making additional funds in yr six of your 30-year mortgage (month 61), you’d solely save $15,095.21, and shed simply 78 months off your mortgage.

Even when you procrastinated for only one yr to provoke the additional $100 cost, your whole financial savings would drop to $20,989.55, and solely eight years would come off your mortgage time period.

Briefly, the sooner you begin making additional funds, the extra you’ll save. That is primarily as a result of mortgage funds are interest-heavy at first of the time period.

[Are biweekly payments a good idea?]

One Further Lump Sum Mortgage Cost

- An additional lump sum mortgage cost may very well be extra useful

- If made quickly after you are taking out your mortgage

- Its worth diminishes over time since much less curiosity is due later within the mortgage time period

- However it may very well be a greater possibility than paying slightly every month

Now let’s assume that you just came across some additional dough and need to make one lump sum cost to cut back your mortgage stability.

Utilizing our identical mortgage particulars from above, when you made a one-time additional cost of $5,000 to principal in month 13, you’d save $10,071.67 and cut back your mortgage time period by 31 months.

Amazingly, this single additional mortgage cost would prevent cash every month for the subsequent 30 years.

Simply take a look at the quantity of curiosity paid every month after the additional mortgage cost is made versus the identical dwelling mortgage with out additional funds under.

As you possibly can see, cost 14 above consists of $310.30 in curiosity, whereas it’s $326.96 for the mortgage with out additional funds.

In month 15, we see the identical disparity, with $309.74 in curiosity versus $326.46. So every month after the additional cost has been made, curiosity financial savings are realized.

Assuming the mortgage time period is 360 months, it’s straightforward to see how the financial savings can actually add up over time.

After all, the borrower who pays additional gained’t should make funds the complete 360 months as a result of they’ll additionally wind up paying off their mortgage forward of schedule.

Now I discussed that paying additional earlier on within the mortgage time period can prevent much more as a result of you possibly can sort out that curiosity expense earlier than you begin paying it off naturally.

For instance, when you made that very same $5,000 additional cost firstly of yr six of the mortgage (as an alternative of the start of yr two), the whole financial savings drop to $7,943.99 and the time period is barely decreased by 27 months.

So once more, it issues whenever you pay additional.

Making an Further Mortgage Cost Every Yr

- Some owners choose to make an additional cost every year

- Maybe associated to a tax refund verify or from a year-end bonus at work

- That is one other good technique to chop your mortgage time period and save a lot of cash

- And make sure that the bonus cash you obtain is put to good use versus spent frivolously

You possibly can additionally make one additional lump sum cost firstly of every yr, maybe after receiving your year-end bonus.

So let’s say you make a $1,000 bonus cost every year in January, beginning in month 13.

That will prevent $19,005.22 in curiosity and shave 85 months (simply over 7 years) off your mortgage time period.

As you possibly can see, there are all varieties of situations that abound right here, and which one you select, if any, is as much as you.

You may argue that mortgage charges are tremendous low-cost, and thus decide that making additional funds now makes little monetary sense.

Or you might be dwelling in your dream dwelling and never too removed from retirement, with the hopes of dwelling “free and clear” sooner relatively than later.

If that’s the case, making the additional funds now could also be very interesting. Refinancing your mortgage to a shorter time period may additionally make loads of sense.

Simply do not forget that plans (all the time) change; owners are more likely to maneuver or refinance their loans versus carrying them to time period.

So whereas the mathematics may excite you, it might not really pan out.

Easy methods to Pay Further on Your Mortgage

In the event you’re trying to pay additional principal in your mortgage, it’s pretty easy. Although there are some things to be aware of to make sure it will get processed appropriately.

In spite of everything, the very last thing you need is a missed or late mortgage cost when trying to avoid wasting cash.

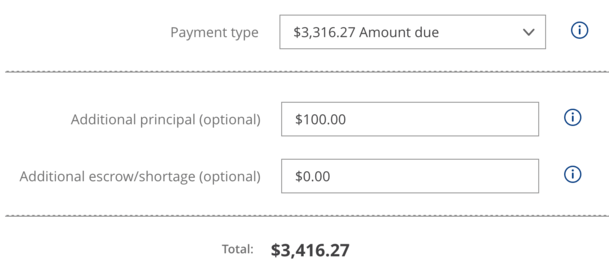

Once you go surfing to make your common mortgage cost, you must see a bit labeled “Extra Funds” or “Extra Principal.”

On this part, you possibly can enter any quantity you’d like past the minimal quantity due, which is your common mortgage cost.

For instance, in case your cost is $3,316.27 per 30 days, you possibly can allocate extra principal together with your cost, say $100.00.

This is able to make your grand whole $3,416.27, with the additional quantity going towards paying down your mortgage stability forward of schedule.

It might prevent curiosity over the remainder of the mortgage time period, but it surely wouldn’t decrease future funds. Any remaining funds would nonetheless be $3,316.27 per 30 days.

Additionally be aware that you just may see the choice to pay additional towards your escrow account, assuming there’s a shortfall or an anticipated one. This has nothing to do with paying your mortgage down quicker.

For these paying by telephone, clarify to the consultant precisely what you’re making an attempt to perform, with any overage going towards the principal stability.

And when you occur to be paying by mail, there is perhaps a bit on the cost coupon relating to extra principal. Merely write within the quantity you need allotted.

What About Partial Mortgage Funds?

An choice to make a partial cost is also listed in your mortgage servicer’s cost web page, however this differs from paying additional.

Sometimes, this selection is for many who are behind on their mortgage and trying to catch up.

And it typically leads to the cash being held apart till sufficient for a full cost is allotted.

For instance, when you make a $1,000 partial cost it is perhaps put in a “suspense account” till the remaining $2,316.27 is distributed (utilizing our identical cost instance from above).

In some instances, the cash may merely be returned to you if it’s not the complete quantity due.

I suppose it is also utilized for biweekly funds, assuming the servicer accepts that association.

The important thing right here is to make sure you make at the very least the minimal cost earlier than paying any additional. And verifying that it’s allotted appropriately.

In the event you’re unsure, it is perhaps greatest to contact your mortgage servicer instantly to substantiate funds are made as anticipated.

Even if you’re “positive,” it may very well be useful to confirm with the servicer earlier than paying any quantity apart from the quantity due.

Learn extra: Do you have to repay the mortgage early?

[ad_2]