[ad_1]

A reader just lately requested, “What mortgage price can I get with my credit score rating?” So I figured I’d attempt to clear up a considerably complicated query.

With mortgage charges not at all-time lows (sigh), debtors trying to refinance a mortgage or buy a house are dealing with an uphill battle.

In the present day, it’s way more frequent on your price to start out with a 6 or 7 versus a 2 or 3. Whereas these increased charges aren’t unhealthy traditionally, the speed of change over the previous few years has been dramatic.

This contrasts these Nineteen Eighties mortgage charges, which had been already excessive earlier than merely transferring even increased.

However regardless of the place mortgage charges are, your credit score rating will play an enormous position in figuring out whether or not you get , common, or not-so-good price.

What you see marketed isn’t at all times what you get, and will in truth be loads increased in case you’ve received marginal credit score scores.

Conversely, you may be capable of rating a below-market price in case you’ve received a wonderful FICO rating.

Let’s discover why that’s so you possibly can set the best expectations and keep away from any disagreeable surprises whenever you lastly converse to a lender.

Mortgage Charges Are Primarily based on Your Credit score Rating

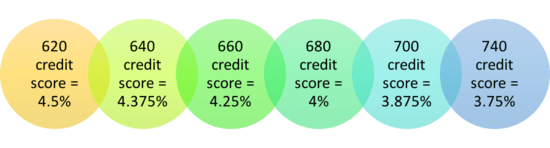

- The illustration above ought to offer you an concept of the significance of credit score scores

- In the case of mortgages even a small distinction in price can equate to 1000’s of {dollars}

- Somebody may have a price 0.75% increased (or extra) based mostly on credit score rating alone

- So make certain all 3 of your credit score scores are as excessive as attainable earlier than you apply!

The graphic above was based mostly on actual marketed charges from Zillow’s market for a $400,000 mortgage quantity at 80% loan-to-value (LTV) for a 30-year mounted on an owner-occupied, single-family residence.

Whereas rates of interest are fairly a bit increased at this time, the identical sliding scale rule applies.

These with increased credit score scores will get the bottom mortgage charges accessible, whereas these with decrease credit score scores must accept increased charges.

Discover that the rate of interest is a full 0.75% increased for a borrower with a 620 FICO rating versus a borrower with a 740+ FICO rating. That may equate to some huge cash over time. And mortgages can final a very long time, generally 30 years!

One factor that determines what mortgage price you’ll finally obtain is credit score scoring, although it’s simply one in all many elements, generally known as mortgage pricing changes, used to find out the value of your mortgage.

Together with credit score scoring is documentation kind, property kind, occupancy kind, mortgage quantity, loan-to-value, and several other others.

Every pricing adjustment is actually utilized based mostly on threat. So a borrower with a high-risk mortgage should pay a better mortgage price than a borrower who presents low threat to the lender.

That is how risk-based pricing works.

Debtors with Decrease Credit score Scores Current Extra Threat to the Lender (And Should Pay Extra!)

Merely put, the much less threat you current to your mortgage lender, the decrease your mortgage price shall be. And vice versa.

That’s as a result of they’ll fetch a better value on your lower-risk residence mortgage once they promote it on the secondary market.

Lenders think about a lot of issues to measure threat, as talked about above.

Utilizing credit score rating alone, it’s not possible to inform a potential borrower what they might qualify for with out realizing all the opposite necessary items of the puzzle.

However I’ll say that your credit score rating is unquestionably probably the most necessary (if not an important) issue that goes into figuring out your mortgage rate of interest.

And as I at all times say, it’s one of many few issues you possibly can largely management. Pay your payments on time, maintain your excellent balances low, and apply for brand spanking new credit score sparingly.

In the event you comply with these easy suggestions, your credit score scores ought to strong. It’s not rocket science.

How A lot Does Credit score Rating Have an effect on the Mortgage Curiosity Price?

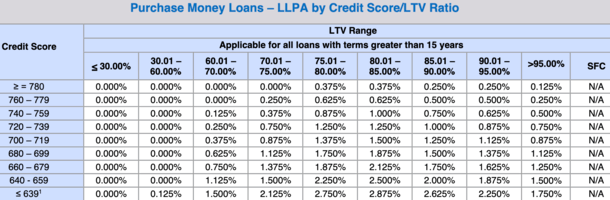

- There are pricing changes particularly for credit score scores

- They’ll increase your mortgage price considerably when you’ve got poor credit score

- The changes develop bigger as credit score scores transfer decrease

- And are particularly impactful in case you additionally are available with a small down fee

Typically talking, a credit score rating of 780 or above ought to land you within the lowest-risk bracket (it was once 740 and earlier than that 720). So it has gotten tougher.

If all different areas of your distinctive borrowing profile are additionally in good standing, you’ll qualify for a mortgage on the lowest attainable rate of interest.

In fact, you’ll have to comparability store to search out that low price too. It received’t essentially come in search of you. However it is best to a minimum of be eligible for the most effective a financial institution or lender has to supply.

This decrease month-to-month mortgage fee will assist you to save on curiosity over the whole mortgage time period.

As talked about, credit score rating might be vastly necessary in figuring out pricing as a result of lenders cost huge changes in case your rating is low.

Simply check out the chart above from Fannie Mae. In case your credit score rating is 780 or increased, you’ll solely be charged 0.375% (this isn’t a price adjustment however somewhat a pricing hit) at 80% LTV (20% down fee).

Conversely, in case your credit score rating is between 640 and 659, you’ll be charged 2.25% in pricing changes.

For the borrower with a 650 credit score rating, this may equate to an rate of interest that’s 0.75% increased on a 30-year mounted mortgage versus the 780-score borrower.

That distinction in price may follow you for years in case you maintain onto your mortgage.

This implies increased funds month after month for many years, all since you didn’t apply good credit score scoring habits.

Not solely can credit score rating prevent cash month-to-month and over time, it can additionally make qualifying for a mortgage loads simpler.

For these causes, your credit score rating needs to be your prime concern when making use of for a mortgage!

What Credit score Rating Do You Want for Finest Mortgage Price?

- Most mortgage price advertisements you’ll come throughout make a lot of assumptions (in case you learn the superb print)

- You’re typically required to have a credit score rating of 740 or increased for the most effective price

- In case your credit score scores aren’t that good, anticipate a better price when acquiring a quote

- Fannie Mae and Freddie Mac now require a 780 FICO rating for the bottom mortgage charges

In the event you’ve ever seen a mortgage commercial on TV or the Web, the lender assumes you’ve received a wonderful credit score rating.

This might imply a credit score rating of 720, 740, or probably even increased. They usually use that assumption to provide a positive mortgage price of their advert.

For instance, Wells Fargo’s mortgage price web page has a disclaimer that reads, “This price assumes a credit score rating of 740.”

However with out that nice credit score rating, your mortgage price could possibly be considerably increased when all is alleged and finished.

And now that Fannie Mae and Freddie Mac have added new credit score scoring tiers, these credit score rating assumptions might rise to 780 for the bottom marketed charges.

Lengthy story quick, goal for 780+ credit score scores any longer if you wish to qualify for the most effective charges.

Debtors With Low Credit score Scores Might Have Hassle Getting Accepted

On the different finish of the spectrum, debtors with credit score scores of say 660, 640, and 620 may have higher difficultly securing a mortgage.

Assuming they’re able to get accepted for a house mortgage, they may obtain increased mortgage charges.

Sadly, I can’t say you’ll get X or Y mortgage price when you’ve got Z credit score rating, there are simply too many elements in play abruptly. And credit score rating is only one of them, albeit a vital one.

However I can say that your credit score rating is vastly influential in figuring out each the mortgage price you’ll obtain and whether or not you’ll efficiently get hold of residence mortgage financing to start with.

So it’s beneficial that you simply examine your credit score rating(s) 3+ months earlier than making use of for a mortgage to see the place you stand. And proceed to observe them up till you apply.

This shouldn’t be a lot of a chore and even an expense now that so many firms present free credit score scores, together with main banks and bank card issuers.

For instance, the numerous banks and bank card firms I do enterprise with supply free scores. And it’s really attention-grabbing to see the divergence in scores throughout completely different firms.

[How to get a mortgage with a low credit score.]

Verify Your Credit score 90+ Days Earlier than Searching for a Mortgage!

- Don’t probability it – examine your credit score scores 3+ months prematurely

- This lets you see the place you stand credit-wise and offers you time to make things better

- It might take months to show issues round if you’ll want to enhance your scores

- Issues like disputes might take 90 days or longer to finish and mirror in your scores

- Goal for a 780 FICO rating to qualify for the most effective mortgage charges

In the event you don’t know your credit score scores a number of months prematurely of making use of for a mortgage, you might not have enough time to make any essential modifications.

Belief me, surprises come up on a regular basis on the subject of credit score.

An misguided (or forgotten) late fee may deflate your credit score scores considerably, even when it’s reporting in error.

And that decrease rating may enhance your mortgage price a proportion level or extra. Sure, credit score scores could make that a lot affect!

Disputing errors and/or addressing different credit score missteps can take many months to finish, so don’t hesitate to examine your credit score in case you suppose you’ll be making use of for a mortgage at any level within the close to future.

It’s good to know the place you stand always, however particularly earlier than making use of for a house mortgage. Don’t simply assume you’ve received glorious credit score. Confirm it!

And when you’re at, don’t make a variety of purchases earlier than making use of for a mortgage. That can also sink your scores.

The excellent news is poor credit score scores might be improved. You’re aren’t caught with them. In case your credit score scores want some TLC, take the time to enhance them as a substitute of settling for a better price at this time.

In case your scores are already glorious, don’t overlook to buy round! Merely evaluating a number of completely different lenders might be simply as necessary as sustaining good credit score.

Learn extra: What credit score rating do I have to get a mortgage?

[ad_2]