[ad_1]

For those who’re new to actual property and making ready to make a suggestion on a property, you may be questioning what mortgage is finest for a first-time residence purchaser.

That is particularly essential now that mortgage charges have basically doubled, placing budgets entrance and middle.

It additionally means the favored 30-year fastened is not the default choice for residence consumers, with cheaper adjustable-rate mortgages now a consideration.

Whereas each seasoned owners and first-time consumers might wind up with the identical actual residence mortgage, there are extra choices to contemplate if you happen to’ve by no means purchased a house earlier than.

Let’s discover the various mortgage decisions out there at this time to find out what may be finest within the present atmosphere.

Residence Mortgage Varieties to Think about If You’re a First-Time Purchaser

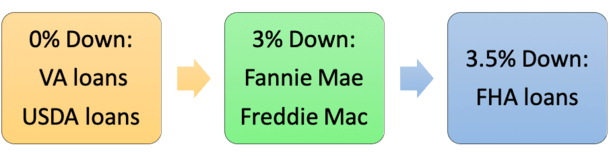

- Fannie Mae HomeReady (3% down fee)

- Freddie Mac Residence Attainable (3% down fee)

- FHA loans (3.5% down fee)

- VA loans (0% down fee for vets/lively responsibility)

- USDA loans (0% down fee for rural residence consumers)

- State Housing Finance Company loans (down fee help and assist with closing prices)

- Additionally search for native and nationwide grants for first-time residence consumers and Mortgage Credit score Certificates (MCCs)

I’ve listed the most typical mortgage sorts out there to first-time residence consumers, a lot of that are additionally an choice for current owners.

These usually don’t require a lot by way of down fee, which appears to be a chief want/need for first-time consumers that don’t have the fairness of move-up consumers.

Personally, I choose to put down 20% on a house buy to keep away from expensive mortgage insurance coverage and to acquire a decrease mortgage price, however I perceive that isn’t at all times lifelike.

If a veteran/lively responsibility, there are VA loans that require 0% down fee and include decrease mortgage charges relative to different mortgage sorts.

If shopping for in a rural space, USDA loans additionally enable 0% down fee and aggressive mortgage charges.

There are fewer restrictions on FHA loans, which require a 3% down fee however enable credit score scores as little as 580.

As well as, conforming loans backed by Fannie Mae and Freddie Mac solely require a 3% down fee.

Word that for Fannie/Freddie loans, you may get your loan-level worth changes (LLPAs) waived if you happen to’re a first-time residence purchaser with qualifying revenue ≤100% space median revenue (AMI) or 120% AMI in high-cost areas.

Or if the mortgage is HomeReady/Residence Attainable, meets Obligation to Serve necessities, is in a excessive wants rural area, a mortgage to a Native American on tribal land, or a mortgage originated by a “small monetary establishment.”

So for these missing property, the applications listed above are in all probability a great start line, particularly if you happen to qualify for LLPA waivers.

Is Your First Residence a Starter Residence or a Ceaselessly Residence?

- All the time take into consideration how lengthy you’ll keep within the property you’re shopping for

- It may be potential to economize by selecting an ARM if you happen to plan on transferring quickly

- Many first-time consumers move-up to bigger properties inside a couple of quick years

- Your anticipated tenure can also be a key consideration with regard to paying factors

When you select a mortgage kind, you possibly can determine on a particular mortgage program, comparable to a 30-year fastened, 15-year fastened, or an ARM.

Whereas most first-time consumers will in the end go together with a 30-year fastened, let’s talk about how the property itself may dictate your financing determination.

The first factor I’d contemplate when shopping for a primary residence can be how lengthy you propose to maintain it. A number of of us purchase what are generally known as “starter properties” initially, then transfer as much as bigger properties inside a couple of years.

For instance, if you happen to simply bought married and need to purchase a house subsequent, you may also be occupied with beginning a household shortly after that.

This typically ends in outgrowing that first residence, and requiring a brand new, bigger property. Relying in your timeline, this might all occur inside only a few years.

In that case, it may make sense to go together with a hybrid adjustable-rate mortgage (ARM) such because the 5/1 ARM or 7/1 ARM.

Whereas fastened mortgage charges aren’t way more costly than ARMs in the meanwhile, this isn’t at all times the case. Typically it’s considerably cheaper to go together with an ARM.

And these hybrid ARMs provide a fixed-rate interval for the primary 5 or seven years earlier than you even have to fret about an rate of interest adjustment.

In different phrases, it operates precisely like a 30-year fixed-rate mortgage up till its first adjustment – by then you can have already bought and moved on to a brand new property.

Tip: It may be simpler to skip the starter residence as a result of entry-level properties are usually essentially the most in demand. You can even keep away from having to maneuver a second time!

Be Conscious About Paying Factors Upfront

One other consideration is whether or not or to not pay mortgage factors – once more, how lengthy you propose on staying has so much to do with it.

These factors are a type of pay as you go curiosity that decrease the rate of interest you obtain in your mortgage. In brief, you pay at this time (at mortgage closing) for a reduction whilst you maintain the mortgage.

For instance, you would possibly pay one level for a 0.375% low cost in price for the following 30 years.

Nevertheless, there’s no level (no pun supposed) in paying factors on a mortgage you’ll solely preserve for a couple of years. Typically it takes a few years to break-even on low cost factors paid.

Even if you happen to keep within the residence, it’s possible you’ll refinance your mortgage sooner fairly than later, making factors a shedding proposition.

Think about the present mortgage price atmosphere, and the place rates of interest might be headed after you purchase.

The exception to this may be a short-term buydown, particularly if it’s paid for by the lender or vendor, because you get the complete worth within the first couple years. Or doubtlessly a refund if you happen to refinance/promote early.

You Don’t Need to Be Home Poor

- You could expertise fee shock or develop into home poor when shopping for your first residence

- This implies going from paying a comparatively small quantity to a big quantity month-to-month

- Additionally contemplate the opposite payments you’ll have to pay like owners insurance coverage and property taxes

- Don’t have a look at the mortgage like a foul debt, it’s typically the most cost effective debt you’ll have the enjoyment of repaying

It might be tempting to go together with a shorter-term mortgage such because the 15-year fastened, seeing that it may well reduce your curiosity expense considerably. However it is going to additionally practically double your month-to-month fee.

One factor mortgage lenders contemplate when extending residence loans to first-time consumers is fee shock.

Merely put, if you happen to go from paying $1,000 monthly in hire to $3,000 on a mortgage, they might fear that you just’ll have a tricky time adjusting to the upper funds.

And so they have good purpose to fret as a result of it’s all supported by information.

Even if you’re authorised for a shorter-term mortgage, it may be higher to take issues sluggish as a substitute of going all-in on the mortgage.

Certain, it’s nice to repay a big debt shortly, however a mortgage generally is a good debt, and is usually the most cost effective debt you’ll have.

Regardless of the 30-year fastened coming in nearer to six.5% or larger at this time, it’s nonetheless comparatively low-cost in comparison with different debt like bank cards and so forth.

And, it’s at all times potential to make further mortgage funds if you wish to pay your mortgage off early, no matter which mortgage program you select.

So you may get the flexibleness of a 30-year mortgage with the choice to prepay it like a 15-year mortgage if you happen to so select.

Test Out Residence Mortgage Packages Solely for First-Time Consumers

- Go to your state’s housing finance company to see what particular applications they provide

- It may be potential to get a mortgage with nothing down if you happen to don’t have a lot cash saved up

- Additionally seek for first-time residence purchaser grants and Mortgage Credit score Certificates which may be out there to you

- Evaluate each conventional and first-time purchaser mortgage applications to find out most suitable choice

Whereas it’s potential to use for any residence mortgage on the market, sure mortgage applications are reserved just for first-time residence consumers.

These are supposed to be extra accommodating to those that might have hassle qualifying, typically as a consequence of down fee.

For those who take a look at your state’s housing finance company (HFA) for homebuyer help, you must see mortgage applications geared particularly towards first-time consumers.

This may embody down fee help, closing value help, or each, helpful if you happen to haven’t saved a lot prior to buy.

One latest instance is the Dream For All Shared Appreciation Mortgage, which doesn’t require a down fee however works as if you happen to put 20% down.

Word: These housing companies aren’t lenders, so that you’ll have to analysis them then use their “discover a mortgage officer” part to see which lenders provide their merchandise.

It’s also possible to do that in reverse if you happen to’re already working with a lender. Ask what HFA applications they provide to first-time residence consumers.

It might even be potential to get a first-time residence purchaser grant with a big financial institution, native credit score union, or direct mortgage lender.

Make sure you seek for native grants as a result of they’re typically forgivable, that means it doesn’t should be paid again!

One instance is the U.S. Financial institution Entry Residence Mortgage, which affords as much as $12,500 in down fee help and a lender credit score as much as $5,000.

The one caveat to a few of these mortgage applications is that you just would possibly want to finish a homeownership class, although it may be helpful and is usually fairly primary and never all that point consuming.

One other perk first-time consumers would possibly have the ability to benefit from is a Mortgage Credit score Certificates (MCC), which might cut back your tax legal responsibility, thereby saving you cash not directly in your mortgage.

It might additionally can help you qualify for a bigger mortgage quantity in some circumstances.

Lastly, look past mortgage applications for first-timers. You could not want any particular mortgage program, and it may truly be cheaper to stay to a conventional one as a substitute.

Who Are the Greatest Mortgage Lenders for First-Time Consumers?

I don’t know of 1 financial institution or lender that focuses on financing for first-time residence consumers, although there are firms that solely cater to residence consumers, comparable to Tomo.

And with mortgage charges considerably larger at this time, most lenders are pivoting to be residence shopping for specialists anyway.

Look out for particular affords and incentives because the mortgage market turns into largely purchase-driven.

Finally, you’ll in all probability discover plenty of the identical mortgage applications irrespective of the place you look, barring a number of the distinctive choices mentioned within the prior part associated to grants and state housing companies.

This implies you’ll have the ability to get an FHA mortgage, USDA mortgage, or VA mortgage from most banks/lenders on the market. The one distinction may be the mortgage charges and/or lender charges.

You also needs to have the ability to acquire a Fannie Mae HomeReady or Freddie Mac Residence Attainable mortgage from nearly any lender.

As famous, each require simply three % down when buying a house and include different potential pricing reductions.

Think about a Mortgage Dealer If You’re a First-Time Residence Purchaser

As a substitute of specializing in a single lender, it may be higher to get in contact with an skilled mortgage dealer, particularly if you happen to’re a first-time purchaser.

These people can information you thru the mortgage course of and examine charges and applications from dozens of lenders directly.

Or construction your mortgage to avoid wasting on mortgage insurance coverage and/or mortgage price with particular down funds.

They are often useful if in case you have plenty of mortgage questions, which is usually the case for somebody buying their very first residence.

You may not get the identical stage of service with a big financial institution or call-center lender.

Alternatively, you possibly can attain out to a HUD-approved housing counselor if you happen to want one-on-one help or are unsure of the place to show for financing.

An skilled actual property agent may additionally be useful, as a lot of them are fairly well-versed in mortgages.

Simply make sure to due your personal diligence and look past their very own suggestions. You don’t have to make use of their “individual.”

Finally, educating your self on mortgages earlier than reaching out to others may be one of the best ways to begin your private home shopping for journey. Being educated means being financially empowered.

Maybe the “finest mortgage” for a first-time residence purchaser is solely one they absolutely perceive.

Learn extra: What is an effective worth for a first-time residence purchaser?

[ad_2]